The medley of regulatory frameworks currently slotting into place across financial markets make it easy to become absorbed in the pressure to meet a succession of deadlines, and to forget the fundamental reason these new initiatives are being enforced.

With so much going on, time is limited for crucial conversations that identify the opportunities arising and explore whether internal systems and processes are still fit-for-purpose.

One such regulation is the Basel Committee on Banking Supervision (BCBS) and the International Organization of Securities Commission (IOSCO) covering initial and variation margin requirements for non-centrally cleared derivatives.

Focusing on variation margin, daily exchange became mandatory for some major market participants on 1 September 2016, and for all other in-scope entities as of 1 March 2017. However, due to the complex logistical constraints in re-papering existing agreements, global regulators issued a ‘no action relief’ until 1 September 2017.

The next phase, scheduled for January 2018, will see foreign exchange (FX) forwards and swaps brought into scope, likely resulting in an exponential increase in the volume of margin calls. This not only places a strain on already-burgeoning workflows, but is also revealing worrying limitations of overburdened, siloed and often legacy technology, which is unable to support change effectively across the buy-side organisation.

Making lemonade

Mark Baker, product manager for collateral management at SimCorp, argues that the incoming margin rules present the buy side with a chance to change and integrate the technology infrastructure, front through back, and claim long-term business benefits that will ultimately affect the bottom line.

“BCBS-IOSCO margin rules mean that collateral management is no longer a periodic back-office function, the new regulation will continue to see it pervading into the front office’s daily workflow,” says Baker.

“The challenges in complying with this new front-to-back regulation, highlight the current limitations and siloed workings of many asset managers’ technology and business infrastructures. If you’re an asset manager and you do it right, compliance does not necessarily mean increased cost. There are overall performance benefits, which may have been previously overlooked, that will come into view, such as empowering the front office with crucial data that is often siloed away in the back-office domain, enhancing pricing, cash and securities forecasting and collateral optimisation.”

Moving target

In a recent survey conducted by SimCorp and Asset Servicing Times, 60 percent of respondents admitted to not being fully ready for the BCBS-IOSCO regulation.

Figure 1

Commenting on the data, Baker notes: “This is unsurprising and certainly mirrors what we have heard from clients and the market at large. Back in March, there was a problem with physically re-papering agreements. The new regulation required updated agreements, but that challenge, for our customers at least, has now been addressed.”

“What we are finding is that firms may have been prepared for the initial implementation, but this regulation has been far from static, hence, readiness is often difficult to define.”

“What is clear is that the inclusion of FX forwards and swaps into the regulatory scope will significantly increase operational workflows and again puts the spotlight on examining existing operating models.”

According to Baker, there are many reasons respondents may be yet to finalise their preparation for the BCBS-IOSCO regulation. Firstly, there are multiple facets to an end-state target operating model, which by their nature will take time to implement. Technology in this respect is both an element and an enabler of change.

Secondly, firms need to be cautious to ensure the change they are making is a long-term solution and not just a short-term fix, to safeguard against internal and external risks.

Those firms taking a truly front-to-back approach will not just be addressing automation and consolidating workflows concerning collateral management, but essentially optimising the entire front-to-back value chain.

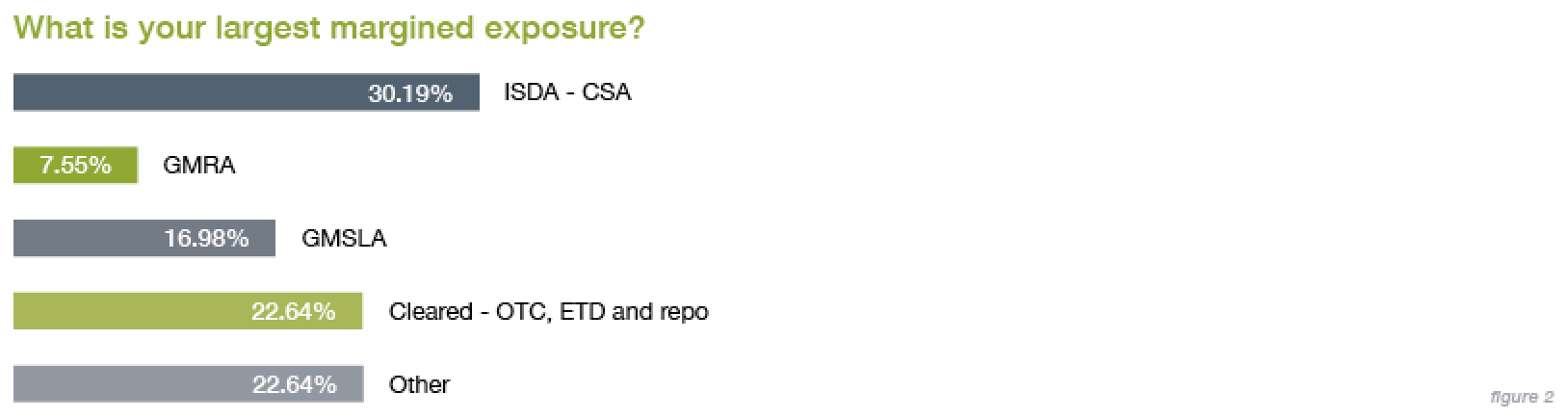

Finally, when looking at margin exposure, the International Swaps and Derivatives Association (ISDA) Credit Support Annex (CSA) is just one of multiple margin call processes undertaken which will need to be optimised by the buy side.

When asked which margin exposure was largest, the ISDA CSA won out for 30 percent of survey respondents, followed by cleared OTC, exchange-traded derivatives, and repo, at just over 22 percent.

Figure 2

Unspecified margin exposure also claimed 22 percent of survey results, with global master securities lending agreements only being the largest exposure for just over 15 percent.

Operating model impacts

Baker divides the impact of the BCBS-IOSCO margin rules on the target operating model into first-order effects and second-order effects.

First and foremost, as of January 2018, buy-side participants must know their processes and underlying technology are sufficiently upgraded to allow them to easily scale processes for agreeing and exchanging margin, either via cash or securities collateral, in an efficient manner.

Adoption of electronic communication that enables automation of the margin call workflow is one example of the way in which both industry and technology are combining to facilitate this drive.

After that, there are second-order effects, as collateral moves up the buy-side value chain. This encompasses business users such as:

Cash and securities managers, who require the ability to forecast potential margin calls and collateral eligibility and ensure access to the appropriate liquidity and collateral, either sourced internally, bilaterally or on a cleared basis;

Risk managers, who must scrutinise and stress market data, liquidity, counterparty and concentration risks into investment and collateral portfolios, including haircuts;

Execution traders, who will require additional analytics as simplistic transaction cost analysis measures may no longer meet updated definitions of best execution; and

Portfolio managers, who require updated pricing models and forecasts of lifetime trade cost to be incorporated into optimal investment strategies.

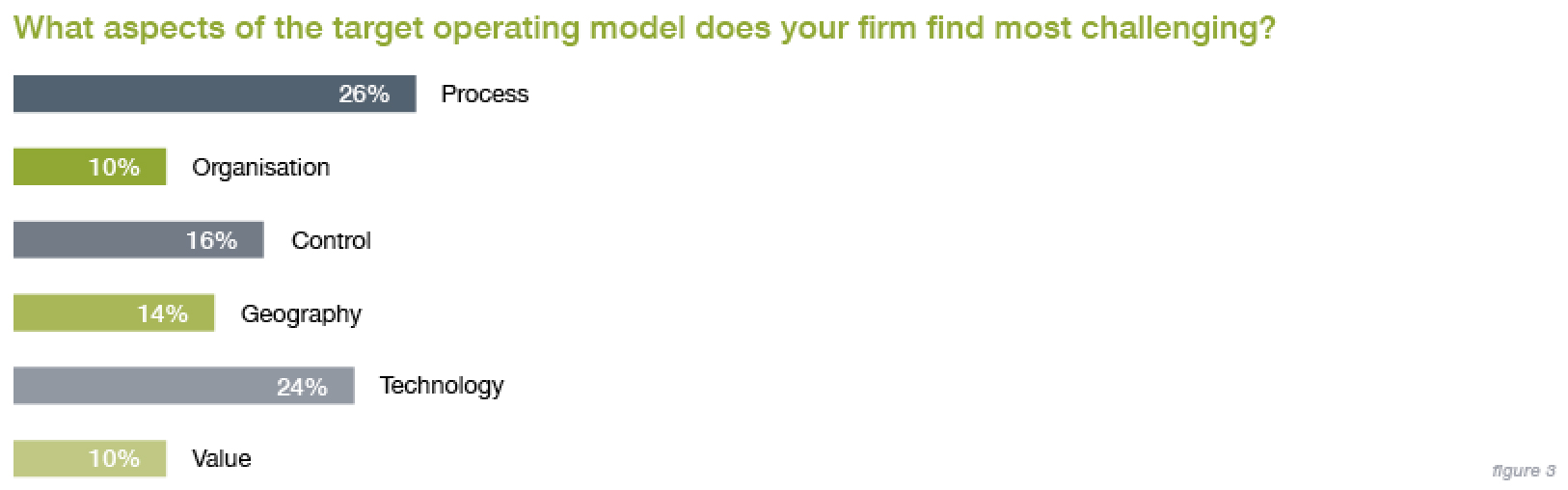

The survey also quizzed respondents on which aspects of their collateral management operating model they found most challenging, with decidedly mixed results.

The data revealed that internal processes created the biggest hurdles, with 26 percent of the vote, followed closely by technology with 24 percent.

Figure 3

Of the remaining responses, 16 percent opted for control, 14 percent chose geography, and value and organisation were selected by 10 percent apiece. According to Baker, the responses “reflect the multi-faceted nature of potential changes to desired target operating models”.

Near-term limitations

The issues of process and technology are inevitably intertwined, and an effective solution to the collateral puzzle requires an adept focus on both. The most effective technology solution will only be as effective as the processes in place to utilise it.

According to SimCorp, an effective collateral management system will adopt automation to alleviate pressure, while also bringing a full front-to-back workflow to process data and manage margins.

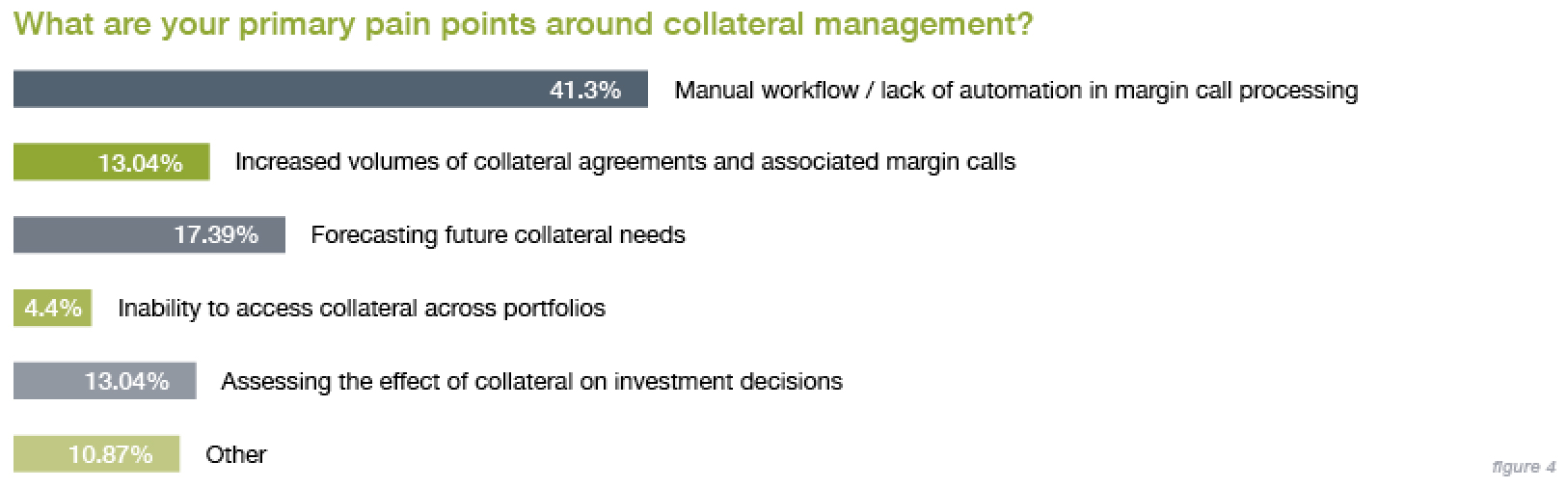

Some buy-side firms appear to be cognisant and proactive on this issue, however, there is a risk that a number are behind the curb, and hence in danger of hitting rough conditions as margin call volumes continue to rise in 2018 and beyond.

Of survey respondents, 41 percent described manual workflows and the lack of automation in margin call processing as their biggest pain point around collateral management.

Figure 4

In fact, issues with automation were the most unifying issue of all surveyed areas of the industry, with the clearest majority in all areas.

Reassuringly, Baker says: “The overall process has evolved, and we are now dealing with some clients on a holistic front-through-back process. It represents a very different workflow for our buy-side clients than we were seeing even as recently as a year ago.”

“From an operations standpoint, our system is looking to automate as much as possible, from optimisation calculations to communications between counterparties. However, for organisational reasons, some processes outside of our system, especially notification flow, stubbornly sit in the manual column.”

To buy or build

In financial markets around the world, the buying-versus-building technology debate has tipped slowly but surely in favour of vendor solutions. For many, it comes down to a question of cost and control. Market trends and regulatory requirements are increasingly demanding transparency and governance of investment data.

With many firms expressing concern over outsourcing of data, and only the largest entities able to build systems in-house, vendor-deployed solutions are looking increasingly attractive.

As it stands, according to the survey, 48 percent of responmdents currently access a vendor stack solution, while 33 percent build internally and 19 percent have trundled along with Excel-driven manual processes.

Figure 5

“Overall, we would expect third-party vendors to have the slight edge in the market split,” says Baker. “Going forward, manual-only processes will be simply unsustainable. Outsourcing will also see a decline, as we continue to hear many firms express concern over lack of timeliness and control of data. I would also question whether in-house builds are truly scalable and cost-efficient in the long run, and whether they are able to maintain and upgrade the technology in the same way a vendor can.”

Beyond the initial need to find a solution to new market challenges, savvy businesses will also have a view to maintaining a wider strategy to ensure seamless processing of transactions throughout their systems. The danger of utilising a patchwork of in-house and outsourced systems is the creation of a network that is unable to communicate effectively.

SimCorp argues that pulling all collateral management processes under a single umbrella is the only way to ensure an efficient workflow.

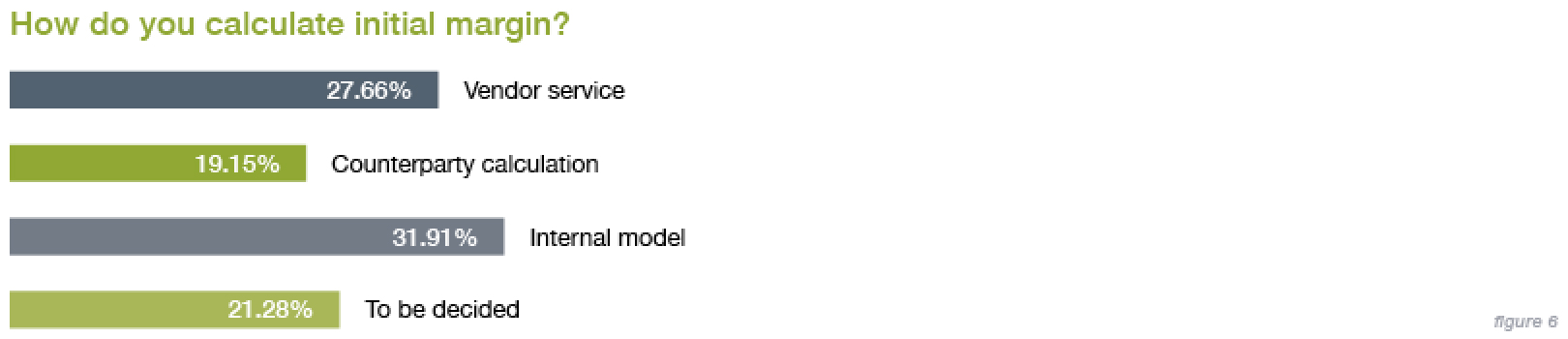

Figure 6

Baker concludes: “The results all point to the need for greater automation and, ultimately, consolidation that allows front and back offices to be unified, for the best way to counteract this issue and future regulations.”

“By making this operational shift, firms are not only complying, but creating opportunities to optimise investment and collateral allocation decisions in one system for both pre and post-trade success.”